The key to building less-expensive batteries that could extend the range of EVs might lie in a cheap, abundant material: sulfur.

Addressing climate change is going to require a whole lot of batteries, both to drive an increasingly electric fleet of vehicles and to store renewable power on the grid. Today, lithium-ion batteries are the dominant choice for both industries.

But as the need for more batteries grows, digging up the required materials becomes more challenging. The solution may lie in a growing number of alternatives that avoid some of the most limited and controversial metals needed for lithium-ion batteries, like cobalt and nickel.

One contender chemistry, lithium-sulfur, could soon reach a major milestone, as startup Lyten plans to deliver limited quantities of lithium-sulfur cells to its first customers later this year. The cells (which can be strung together to build batteries of different sizes) will go to customers in the aerospace and defense industries, a step on the journey to building batteries that can stand up to the test of EVs.

When it comes to new options for batteries, “we need something that we can make a lot of, and make it quickly. And that’s where lithium-sulfur comes in,” says Celina Mikolajczak, chief battery technology officer at Lyten.

Sulfur is widely abundant and inexpensive—a major reason that lithium-sulfur batteries could come with a much cheaper price tag. The cost of materials is around half that of lithium-ion cells, Mikolajczak says.

That doesn’t mean the cost for the new batteries will immediately be lower, though. Lithium-ion has had decades to slowly cut costs, as production has scaled and companies have worked out the kinks. But a lower cost of materials means the potential for cheaper batteries in the future.

Not only could lithium-sulfur batteries eventually provide a cheaper way to store energy—they could also beat out lithium-ion on a crucial metric: energy density. A lithium-sulfur battery can pack in nearly twice the energy as a lithium-ion battery of the same weight. That could be a major plus for electric vehicles, allowing automakers to build vehicles that can go farther on a single charge without weighing them down.

However, there are still major technical barriers Lyten needs to overcome for its products to be ready to hit the road in an EV. Chief among them is getting batteries to last.

Today’s lithium-ion batteries built for EVs can last for 800 cycles or more (meaning they can be sapped and recharged 800 times). Lithium-sulfur options tend to degrade much faster, with many efforts today hovering somewhere around 100 cycles, says Shirley Meng, a battery researcher at the University of Chicago and Argonne National Laboratory.

That’s because taming the chemical reactions that power lithium-sulfur batteries has proved to be a challenge. Unwanted reactions between lithium and sulfur can sap the life out of batteries and drive them to an early grave.

Lyten is far from the first to go after the promise of lithium-sulfur batteries, with companies big and small making forays into the chemistry for decades. Some, like UK-based Oxis Energy, have shuttered, while others, including Sion Power, have pivoted away from lithium-sulfur. But growing demand for alternatives, and a higher level of interest and funding, could mean that Lyten succeeds where earlier efforts have failed, Meng says.

Lyten has made progress in stretching the lifetime of its batteries, recently seeing some samples reach as high as 300 cycles, Mickolajczak says. She attributes the success to Lyten’s 3D graphene material, which helps prevent unwanted side reactions and boost the cell’s energy density. The company is also looking to use 3D graphene, a more complicated structure than the two-dimensional variety, in other products like sensors and composites.

Even with recent progress, Lyten is still far from producing batteries that can last long enough to power an EV. In the meantime, the company plans to bring its cells to market in places where lifetime isn’t quite so important.

Since lithium-sulfur batteries can be extremely lightweight, the company is working with customers building devices like drones, for which replacing the batteries frequently would be worth the savings on weight, says Keith Norman, Lyten’s chief sustainability officer.

The company opened a pilot manufacturing line in 2023 with a maximum capacity of 200,000 cells annually. It recently began producing a small number of cells, which are scheduled for delivery to paying customers later this year.

The company hasn’t publicly shared which companies will receive the first batteries. Moving forward, two of the company’s main focuses are improving lifetime and scaling production of both 3D graphene and battery cells, Norman says.

The road to lithium-sulfur batteries that can power EVs is still a long one, but as Mikolajczak points out, today’s staple chemistry, lithium-ion, has improved leaps and bounds on cost, lifetime, and energy density in the years that companies have been working to tweak it.

People have tried out a massive range of chemistry options in batteries, Mikolajczak says. “To make one of them reality requires that you put in the work.”

MIT Technology Review Explains: Let our writers untangle the complex, messy world of technology to help you understand what’s coming next. You can read more from the series here.

For more than a century, the prevalent image of power plants has been characterized by towering smokestacks, endless coal trains, and loud spinning turbines. But the plants powering our future will look radically different—in fact, many may not have a physical form at all. Welcome to the era of virtual power plants (VPPs).

The shift from conventional energy sources like coal and gas to variable renewable alternatives such as solar and wind means the decades-old way we operate the energy system is changing.

Governments and private companies alike are now counting on VPPs’ potential to help keep costs down and stop the grid from becoming overburdened.

Here’s what you need to know about VPPs—and why they could be the key to helping us bring more clean power and energy storage online.

What are virtual power plants and how do they work?

A virtual power plant is a system of distributed energy resources—like rooftop solar panels, electric vehicle chargers, and smart water heaters—that work together to balance energy supply and demand on a large scale. They are usually run by local utility companies who oversee this balancing act.

A VPP is a way of “stitching together” a portfolio of resources, says Rudy Shankar, director of Lehigh University’s Energy Systems Engineering, that can help the grid respond to high energy demand while reducing the energy system’s carbon footprint.

The “virtual” nature of VPPs comes from its lack of a central physical facility, like a traditional coal or gas plant. By generating electricity and balancing the energy load, the aggregated batteries and solar panels provide many of the functions of conventional power plants.

They also have unique advantages.

Kevin Brehm, a manager at Rocky Mountain Institute who focuses on carbon-free electricity, says comparing VPPs to traditional plants is a “helpful analogy,” but VPPs “do certain things differently and therefore can provide services that traditional power plants can’t.”

One significant difference is VPPs’ ability to shape consumers’ energy use in real time. Unlike conventional power plants, VPPs can communicate with distributed energy resources and allow grid operators to control the demand from end users.

For example, smart thermostats linked to air conditioning units can adjust home temperatures and manage how much electricity the units consume. On hot summer days these thermostats can pre-cool homes before peak hours, when air conditioning usage surges. Staggering cooling times can help prevent abrupt demand hikes that might overwhelm the grid and cause outages. Similarly, electric vehicle chargers can adapt to the grid’s requirements by either supplying or utilizing electricity.

These distributed energy sources connect to the grid through communication technologies like Wi-Fi, Bluetooth, and cellular services. In aggregate, adding VPPs can increase overall system resilience. By coordinating hundreds of thousands of devices, VPPs have a meaningful impact on the grid—they shape demand, supply power, and keep the electricity flowing reliably.

How popular are VPPs now?

Until recently, VPPs were mostly used to control consumer energy use. But because solar and battery technology has evolved, utilities can now use them to supply electricity back to the grid when needed.

In the United States, the Department of Energy estimates VPP capacity at around 30 to 60 gigawatts. This represents about 4% to 8% of peak electricity demand nationwide, a minor fraction within the overall system. However, some states and utility companies are moving quickly to add more VPPs to their grids.

Green Mountain Power, Vermont’s largest utility company, made headlines last year when it expanded its subsidized home battery program. Customers have the option to lease a Tesla home battery at a discounted rate or purchase their own, receiving assistance of up to $10,500, if they agree to share stored energy with the utility as required. The Vermont Public Utility Commission, which approved the program, said it can also provide emergency power during outages.

In Massachusetts, three utility companies (National Grid, Eversource, and Cape Light Compact) have implemented a VPP program that pays customers in exchange for utility control of their home batteries.

Meanwhile, in Colorado efforts are underway to launch the state’s first VPP system. The Colorado Public Utilities Commission is urging Xcel Energy, its largest utility company, to develop a fully operational VPP pilot by this summer.

Why are VPPs important for the clean energy transition?

Grid operators must meet the annual or daily “peak load,” the moment of highest electricity demand. To do that, they often resort to using gas “peaker” plants, ones that remain dormant most of the year that they can switch during in times of high demand. VPPs will reduce the grids’ reliance on these plants.

The Department of Energy currently aims to expand national VPP capacity to 80 to 160 GW by 2030. That’s roughly equivalent to 80 to 160 fossil fuel plants that need not be built, says Brehm.

Many utilities say VPPs can lower energy bills for consumers in addition to reducing emissions. Research suggests that leveraging distributed sources during peak demand is up to 60% more cost effective than relying on gas plants.

Another significant, if less tangible, advantage of VPPs is that they encourage people to be more involved in the energy system. Usually, customers merely receive electricity. Within a VPP system, they both consume power and contribute it back to the grid. This dual role can improve their understanding of the grid and get them more invested in the transition to clean energy.

What’s next for VPPs?

The capacity of distributed energy sources is expanding rapidly, according to the Department of Energy, owing to the widespread adoption of electric vehicles, charging stations, and smart home devices. Connecting these to VPP systems enhances the grid’s ability to balance electricity demand and supply in real time. Better AI can also help VPPs become more adept at coordinating diverse assets, says Shankar.

Regulators are also coming on board. The National Association of Regulatory Utility Commissioners has started holding panels and workshops to educate its members about VPPs and how to implement them in their states. The California Energy Commission is set to fund research exploring the benefits of integrating VPPs into its grid system. This kind of interest from regulators is new but promising, says Brehm.

Still, hurdles remain. Enrolling in a VPP can be confusing for consumers because the process varies among states and companies. Simplifying it for people will help utility companies make the most of distributed energy resources such as EVs and heat pumps. Standardizing the deployment of VPPs can also speed up their growth nationally by making it easier to replicate successful projects across regions.

“It really comes down to policy,” says Brehm. “The technology is in place. We are continuing to learn about how to best implement these solutions and how to interface with consumers.”

The motor in your vacuum cleaner and the one in your electric vehicle likely have at least one thing in common: they both rely on powerful permanent magnets to function. And the materials for those magnets could soon be in short supply.

Permanent magnets can maintain a magnetic field on their own without an electric charge. They’re commonly used in motors, making them spin when an electric field is applied. The permanent magnets used in high-end motors today are built using a class of materials called rare earth metals. Demand for these materials is expected to skyrocket in the coming decades, fueled in particular by the growth of electric vehicles and wind turbines. As mines and processing facilities struggle to keep up, supplies may stretch thin.

One Minnesota startup has been working to address this looming shortage. Niron Magnetics is building a large-scale manufacturing facility to produce iron nitride, a magnetic material derived from common elements, while also working to improve the material’s properties so that it can be used in stronger magnets to power more products. The results may help address yet another coming supply crunch that threatens to slow down action on climate change.

A growing gap

The permanent magnets you’re probably most familiar with are the cheap ones made from materials called ferrites that are holding up postcards and wedding announcements on your refrigerator.

But many of the devices sprinkled through our daily lives, like our vacuums and EVs, require much higher-powered magnets. Motors that generate motion using permanent magnets tend to be more powerful and efficient, so rare earth metals, such as neodymium and dysprosium, have become vital for a wide range of devices. In a wind turbine, for instance, magnets in the generator harness motion from the blades and turn it into electricity.

Like many of the other materials needed for clean energy technologies, we can expect a meteoric rise in demand for rare earth metals used in magnets as the world rushes to address climate change.

In the case of neodymium and dysprosium, supply will need to increase sevenfold by 2050 just to meet demand for wind turbines, says Seaver Wang, co-director of the climate and energy team at the Breakthrough Institute, an environment and policy think tank.

In addition, rare earth metal demand for electric vehicles could increase 15-fold from today’s levels by 2040, according to an analysis from the International Energy Agency. And it’s not just clean energy technologies—increased access to electricity and cheap electronics means demand for rare earth metals will rise across other sectors, too.

The world is unlikely to exhaust the geological reserves of rare earth metals anytime soon, Breakthrough’s Wang says—rare earth metals aren’t actually all that rare, at least when it comes to the entire planet’s supply. But they don’t tend to be very concentrated even in the places they are found, so scaling the supply of rare earth metals quickly and economically enough will be a major challenge.

In the near term, global demand for magnets made with neodymium could triple by 2035, while production will likely only double by then, given the long lead times required to build new mines, according to materials research firm Adamas Intelligence.

Given the growing demand, “the world needs a different solution and technology,” says Jonathan Rowntree, CEO of Niron Magnetics.

Few alternatives to permanent magnets exist today. Recycling can help reduce the need for future rare earth mining and processing, but there won’t be enough used material to meet the growing demand for decades.

Rowntree and his colleagues see iron nitride as part of the solution to the anticipated problem of constraints in the supply of rare earth metals. Iron nitride magnets don’t use those metals, and they don’t require cobalt, another metal sometimes used in magnets (and in lithium-ion batteries) that’s under growing scrutiny because of the environmental and humanitarian issues often associated with its mining. And some experts say these iron-based materials might end up creating magnets just as strong as those that include rare earth metals.

An attractive alternative

Though iron nitride (specifically, a phase called alpha double prime) was discovered in the 1950s, it wasn’t until the 1970s that researchers discovered its strong magnetic properties, says Jian-Ping Wang, a professor at the University of Minnesota and the technical founder and chief scientist at Niron Magnetics.

Even then, scientists couldn’t explain the physics underlying the material’s magnetic properties, and they struggled to recreate magnetic samples reliably through the 1990s. Intrigued by this problem, Wang began work on iron nitride materials at the university in 2002.

After making hundreds of samples and working for nearly a decade, Wang cracked the code to reliably make iron nitride materials in thin films. He presented his findings at a major conference in 2010, the same year geopolitical tensions between Japan and China sparked a huge increase in the price of rare earth metals.

Suddenly, there was a greater appetite for alternatives to rare earths that could be used to make strong permanent magnets. The US Department of Energy’s ARPA-E office sponsored grants to develop such materials, awarding one to Wang and the research that would eventually become Niron Magnetics.

Rare earth metals became ubiquitous across technologies because they represented “a huge jump” in the energy density of magnets when they were discovered in the 1960s, says Matthew Kramer, a senior scientist at Ames National Laboratory.

One of the primary gauges of a magnet’s properties is its energy density, measured in mega-gauss-oersteds (MGOe). While the ferrite magnets on your fridge likely have an MGOe of around 5, neodymium-based magnets are much stronger, reaching around 50 MGOe.

Rare earth metals like neodymium are currently a crucial ingredient in permanent magnets because they can wrangle other metals into an arrangement that helps generate a strong magnetic field.

Permanent magnets produce magnetic fields because of spinning electrons, small charged particles in atoms. Different elements have different numbers of free electrons that in some circumstances can be made to spin in the same direction, generating a magnetic field. The more electrons that are free and spinning in the same direction, the stronger the magnetic field.

Iron has a lot of free electrons, but without an overarching structure they tend to spin in different directions, canceling each other out. Adding in neodymium, dysprosium, and other rare earth metals can help arrange iron atoms in a way that allows their electrons to work together, resulting in powerful magnets.

Iron nitride does what few other materials can: it arranges iron into a structure that gets electrons spinning together in this way and keeps them aligned—no rare earth metals required.

“If you could get the nitrogen to spread these irons out in the appropriate way, you should be able to potentially get a really, really good permanent magnet,” Kramer says. That has proven to be a challenge though, he adds, because it’s difficult to make these materials in bulk and to harness the complex chemistry in a way that forces them to retain their magnetization.

Idea to execution

After Wang was able to reliably create thin films of iron nitride, the next step was to figure out how to make it in bulk, grind it up, and squish it together to make magnets.

Finding a manufacturing process was a challenge in part because iron nitride degrades at high temperatures, which limits the options available in traditional magnet manufacturing, Wang explains. He developed several methods to make iron nitride in bulk, one of the most promising of which involves diffusing nitrogen through iron oxide (rust is a type of iron oxide) under very specific conditions.

In recent years, Niron has focused on perfecting and scaling up the manufacturing process, Rowntree says. A significant remaining challenge is determining how to help iron nitride reach its full potential.

NIRON MAGNETICS

In theory, iron nitride should be able to produce magnets that are even stronger than neodymium ones. But today, Niron’s magnets can only reach around 10 MGOe, Rowntree says. That’s sufficient for devices like speakers, which the company is exploring as an early product. It displayed small speakers made with Niron magnets at CES in January.

With higher magnet strength, iron nitride magnets will be more useful in devices like electric vehicles and wind turbines. In theory, the material should be able to reach 20 to 30 MGOe using Niron’s current manufacturing method, Wang says, though achieving that will require “a lot of optimization.” The theoretical ceiling is much higher, with iron nitride potentially being able to form magnets stronger than the neodymium ones used today.

Niron recently received over $30 million from investors, including GM Ventures and Stellantis Ventures, for a total of more than $100 million in funding. The company is working to scale up production capacity in its current pilot plant, with the aim of reaching 1,000 kilograms of production capacity by the end of 2024.

Niron’s work, along with other alternatives and workarounds, could be crucial in loosening a major potential bottleneck for several critical climate technologies.

“Increased magnets and increased magnet supply are critical to enabling the energy transition,” says Gregg Cremer, an advisor at ARPA-E. “Without more magnets, we’re just not going to be able to meet our objectives.”

This article is from The Spark, MIT Technology Review’s weekly climate newsletter. To receive it in your inbox every Wednesday, sign up here.

The potential to use old, discarded products to make something new sounds a little bit like magic. I absolutely understand the draw, and in some cases, recycling is going to be a crucial tool for climate technology. I’ve written about recycling for basically any climate technology you can think of, including solar panels, wind turbines, and batteries. (I’ve also covered efforts to recycle plastic waste.)

For my most recent story, I was researching the materials used for the magnets that power EVs and wind turbines. (Read the result here!) And once again, I was struck by a stark reality: there are massive challenges ahead in material demand for climate technologies, and unfortunately, recycling alone won’t be enough to address them. Let’s take a look at why recycling isn’t always the answer, and what else might help.

Mind the gap

We’re building a whole lot more climate technologies than we used to, which means there aren’t enough old, discarded technologies sitting around, waiting to be mined for materials. Obviously the growth in clean-energy technologies is a great thing for climate action. But it presents a problem for recycling.

Take solar panels, for instance. They tend to last at least 25, maybe 30 years before they start to lose the ability to efficiently harness energy from the sun and transform it into electricity. So the panels available for recycling today are those that were installed over two decades ago (a relatively small fraction are ones that have been broken or need to be taken down early).

In 2000, there was a little over one gigawatt of solar power installed globally. (Yes, 2000 was nearly 25 years ago—sorry!) So today’s recycling companies are competing with each other for that relatively small amount of material. If they can hang in there, there will eventually be plenty of solar panels to go around. Over 300 gigawatts of solar power were added in 2023.

This gap is a common challenge in recycling for other technologies, too. In fact, one of the problems facing the growing number of battery recycling companies is a looming shortage of materials to recycle.

It’s important to start building infrastructure now, so we’re ready for the inevitable wave of solar panels and batteries that will eventually be ready for recycling. In the meantime, recyclers can get creative in where they’re sourcing materials. Battery recyclers today will rely on a lot of manufacturing scrap. Looking to other products can help as well—rare earth metals for EV motors and wind turbines could be partially sourced from old iPhones and laptops.

Closing the loop

Even if we weren’t seeing explosive growth for new technologies, there would be another problem: no recycling process is perfect.

The issues start at the stage of collecting old materials (think of the iPods and flip phones in your junk drawer, gathering dust), but even once material makes it to a recycling center, some will wind up in the waste because it breaks down in the process or just can’t be economically recovered.

Exactly how much material can be recovered depends on the material, the recycling process, and the economics at play. Some metals, like the silver in solar cells, might be able to reach 99% recovery or higher. Others can pose harder challenges, including the lithium in batteries—one recycler, Redwood Materials, told me last year its process can recover around 80% of the lithium from used batteries and manufacturing scrap. The rest will be lost.

I don’t mean to be a Debbie Downer. Even with imperfect recovery, recycling could help meet demand for materials in many energy technologies in the future. Recycling rare earth metals could cut mining for metals like neodymium in half, or more, by 2050.

But a robust supply of recycled materials for many climate technologies is still decades away. In the meantime, many companies are working to build options that use more widely available, cheaper alternatives. Check out my story on one startup, Niron Magnetics, which is working to build permanent magnets without rare earth metals, to see how new materials can help accelerate climate action and close the gap that recycling leaves.

The world’s largest EV maker is getting into the shipping business. BYD is amassing a fleet of ships to export its vehicles from China to the rest of the world. Read more about why the automaker is getting creative and what comes next in this fascinating story from my colleague Zeyi Yang.

The world’s largest cruise ship departed on its maiden voyage last week. The whole thing is a bit of a climate fiasco. Taking a cruise can be about twice as emissions intensive as flying and staying in a hotel. (Bloomberg)

A new refinery in Georgia will churn out millions of tons of jet fuel made from plants instead of petroleum. The new facility marks a milestone for alternative jet fuels. (Canary Media)

→ While alternatives are often called “sustainable aviation fuels” or SAFs, some varieties are anything but sustainable. Here’s what you need to know about all these newfangled jet fuels. (MIT Technology Review)

China nearly quadrupled its new energy storage capacity last year. It’s a massive jump for the growing industry, which is key to balancing the growing fraction of renewables on the grid. (Bloomberg)

Huge charging depots for electric trucks are coming to California. Big batteries in big vehicles require big chargers, and new funding from the US government could be crucial in building them. (Canary Media)

→ The three biggest truck makers are calling for better charging infrastructure for heavy-duty vehicles (New York Times)

EV charging can get a bit tricky for those of us who don’t live in single-family homes with a garage to charge in. Here are some solutions. (Washington Post)

The US is the world’s largest exporter of liquefied natural gas, but new exports are on pause. The Department of Energy says it’s trying to work out how to regulate them, and what the climate impact of cutting gas exports might be. (Grist)

This article is from The Spark, MIT Technology Review’s weekly climate newsletter. To receive it in your inbox every Wednesday, sign up here.

The world is building solar panels, wind turbines, electric vehicles, and other crucial climate technologies faster than ever. As the pace picks up, though, a challenge is looming: we need a whole lot of materials to build it all.

From cement and steel to nickel and lithium, the ingredient list for the clean energy transition is a long one. And in some cases, getting our hands on all those materials won’t be simple, and the trade-offs are starting to become abundantly clear.

My colleague James Temple, senior editor for energy here at MIT Technology Review, has spent over a year digging into the building tensions around mining for critical minerals. In a new story published this week, James highlights one community in rural Minnesota and the conflicts over a mining project planned for the nearby area.

If you haven’t already, I highly recommend you check out that article. In the meantime, I got to sit down with James to ask him a few questions about the process of reporting and writing this feature and chat about critical minerals and the energy transition. Here’s some of what we talked about.

So, what’s the big deal with critical minerals?

To address climate change, “we just need to build an enormous amount of stuff,” James says. And building all of it means a whole lot of demand for materials.

We might need nearly 20 times more nickel in 2040 than the annual supply in 2020, according to the International Energy Agency. That multiple is 25 times for graphite, and for lithium it’s over 40 times the current figure.

Even if people agree in the abstract that we need to extract and process the materials needed to build the stuff to address climate change, figuring out where it all should come from is easier said than done. “We came to realize that mining proposals were creating community tensions basically anywhere they appeared in the US,” James says.

There’s pushback to all sorts of different climate tech projects—we’ve seen very vocal opposition to proposed wind farms, for example. But there seems to be an additional layer to the concerns around mining, James says. Among other reasons, it’s a legacy industry with a particularly checkered past in terms of environmental impact.

Even as communities raise concerns over new mining projects, “you also saw the companies proposing them stressing the potential benefits to cleantech and climate goals,” James says. This combination of clear potential climate benefits with community concerns was worth exploring, he tells me.

What does a proposed nickel mine near a small town in Minnesota tell us about conflict over critical minerals?

The town of Tamarack, Minnesota, has a population of around 70.

Despite its small size, Tamarack could soon be key to a crucial landmark for climate technology, because Talon Metals wants to build a huge mine outside the town that could dig up as much as 725,000 metric tons of raw ore each year. The primary target is nickel, a metal that’s crucial to building high-performance EV batteries.

Talon has been very explicit in claiming that this mine would have benefits for the planet, going as far as applying to trademark the term “Green Nickel.” That’s one of the reasons this particular site piqued James’s interest, he says.

At the same time, local concerns are growing. Drilling could release 2.6 million gallons of water into the mine every day, which Talon plans to pump out and treat before it’s released into nearby wetlands. This part of the plan has caused some of the greatest unease, since local fresh water is crucial to the community’s economy and identity.

The central tension was abundantly clear on a nearly weeklong trip to Tamarack and the surrounding communities, James tells me. He went to Rice Lake National Wildlife Refuge and learned about native wild rice that grows there and its importance to Indigenous groups. He went to see samples of the ore that Talon dug up and spoke to a geologist about the resources in the region. He also attended community meetings that got a little heated, and even had to contend with some local bees.

“We’re talking about a story of two different, very precious resources that have created a really difficult-to-address conflict,” he says. “It’s a tension that’s ultimately going to be very hard to resolve.”

There are rarely easy answers when it comes to the massive task of addressing climate change. If you’re interested in getting a better understanding of this complicated web of trade-offs, take the time to read James’s story. You’ll get all the details about why this particular deposit is such a big deal, and hear more about where things are likely to go from here.

And the story doesn’t stop there. James also has another big project out this week, in which he worked to understand how this one mine could unlock billions of dollars in government subsidies. Dig into that here.

Some truck drivers are falling in love with EVs. Electric trucks are still limited in range, and they make up a small fraction of the trucks on the road, but drivers are starting to see the upside, even as critics say the move to electric is going too fast. (Washington Post)

Gas prices are down in the US, but charging up an EV is still way cheaper. Here’s how cheap gas has to get in every state to compete with EV charging. (Yale Climate Connections)

Old cell phones might provide a much-needed source of rare earth metals. These metals are crucial for motors, including the ones in electric vehicles and wind turbines, and recycling could meet as much as 40% of US demand by 2050. (New York Times)

→ Old personal devices can be a source for other metals, like lithium and cobalt, as I wrote in this story on battery recycling from last year. (MIT Technology Review)

Nobody knows when the next nuclear plant will come online in the US. The former front-runner was a NuScale modular reactor array, but the future of that project is uncertain now. (Canary Media)

Local bans can eliminate nearly 300 single-use plastic bags per person per year, according to a new report. Bottom line: the policies work. (Grist)

Europe will need 34,000 miles (54,000 kilometers) of additional transmission lines to handle the growth in offshore wind power. It could be Europe’s third-biggest energy source by 2050, if infrastructure can keep up. (Bloomberg)

This article is from The Spark, MIT Technology Review’s weekly climate newsletter. To receive it in your inbox every Wednesday, sign up here.

I’ve got nuclear power on the brain this week.

The workings of nuclear power plants have always fascinated me. They’re massive, technically complicated, and feel a little bit magic (splitting the atom—what a concept). But I’ve reached new levels of obsession recently, because I’ve spent the past week or so digging into advanced nuclear technology.

Advanced nuclear is a mushy category that basically includes anything different from the commercial reactors operating now, since those basically all follow the same general formula. And there’s a whole world of possibilities out there.

I was mostly focused on the version that’s being developed by Kairos Power for a story (which was published today, check it out if you haven’t!). But I went down some rabbit holes on other potential options for future nuclear plants too. So for the newsletter this week, let’s take a peek at the menu of options for advanced nuclear technology today.

The basics

Before we get into the advanced stuff, let’s recap the basics.

Nuclear power plants generate electricity via fission reactions, where atoms split apart, releasing energy as heat and radiation. Neutrons released during these splits collide with other atoms and split them, creating a chain reaction.

In nuclear power plants today, there are basically two absolutely essential pieces. First, the fuel, which is what feeds the reactions. (Pretty obvious why this one is important.) Second, it’s vital that the chain reactions happen in a controlled manner, or you can get into nuclear meltdown territory. So the other essential piece of a nuclear plant is the cooling system, which keeps the whole thing from getting too hot and causing problems. (There’s also the moderator and a million other pieces, but let’s stick with two so you’re not reading this newsletter all day.)

In the vast majority of reactors on the grid today, these two components follow the same general formula: the fuel is enriched uranium that’s packed into ceramic pellets, loaded into metal pipes, and arranged into the reactor’s core. And the cooling system pumps pressurized water around the reactor to keep the temperature controlled.

But for a whole host of reasons, companies are starting to work on making changes to this tried-and-true formula. There are roughly 70 companies in the US working on designs for advanced nuclear reactors, with six or seven far enough along to be working with regulators, says Jessica Lovering, cofounder and co-executive director at the Good Energy Collective, a policy research organization that advocates for the use of nuclear energy.

Many of these so-called advanced technologies were invented and even demonstrated over 50 years ago, before the industry converged on the standard water-cooled plant designs. But now there’s renewed interest in getting alternative nuclear reactors up and running. New designs could help improve safety, efficiency, and even cost.

Coolant

Alternative coolants can improve on safety over water-based designs, since they don’t always need to be kept at high pressures. Many can also reach higher temperatures, which can allow reactors to run more efficiently.

Molten salt is one leading contender for alternative coolants, used in designs from Kairos Power, Terrestrial Energy, and Moltex Energy. These designs can use less fuel and produce waste that’s easier to manage.

Other companies are looking to liquid metals, including sodium and lead. There are a few sodium-cooled reactors operating today, mainly in Russia, and the country is also at the forefront in developing lead-cooled reactors. Metal-cooled reactors share many of the potential safety benefits of molten-salt designs. Helium and other gases can also be used to reach higher temperatures than water-cooled systems. X-energy is designing a high-temperature gas-cooled reactor using helium.

Fuel

Most reactors that use an alternative coolant also use an alternative fuel.

TRISO, or tri-structural isotropic particle fuel, is one of the most popular options. TRISO particles contain uranium, enclosed in ceramic and carbon-based layers. This keeps the fuel contained, keeping all the products of fission reactions inside and allowing the fuel to resist corrosion and melting. Kairos and X-energy both plan to use TRISO fuel in their reactors.

Other reactors use HALEU: high-assay low-enriched uranium. Most nuclear fuel used in commercial reactors contains between 3% and 5% uranium-235. HALEU, on the other hand, contains between 5% and 20% uranium-235, allowing reactors to get more power in a smaller space.

Size

I know I said I’d keep this to two things, but let’s include a bonus category. In addition to changing up the specifics of things like fuel and coolant, many companies are working to build reactors of different (mostly smaller) sizes.

Today, most reactors coming on the grid are massive, in the range of 1,000 or more megawatts—enough to power hundreds of thousands of homes. Building those huge projects takes a long time, and each one requires a bespoke process. Small modular reactors (SMRs) could be easier to build, since the procedure is the same for each one, allowing them to be manufactured in something resembling a huge assembly line.

NuScale has been one of the leaders in this area—its reactor design uses commercial fuel and water coolant, but the whole thing is scaled down. Things haven’t been going so well for the company in recent months, though: its first project is pretty much dead in the water, and it laid off nearly 30% of its employees in early January. Other companies are still carrying the SMR torch, including many that are also going after alternative fuels and coolants.

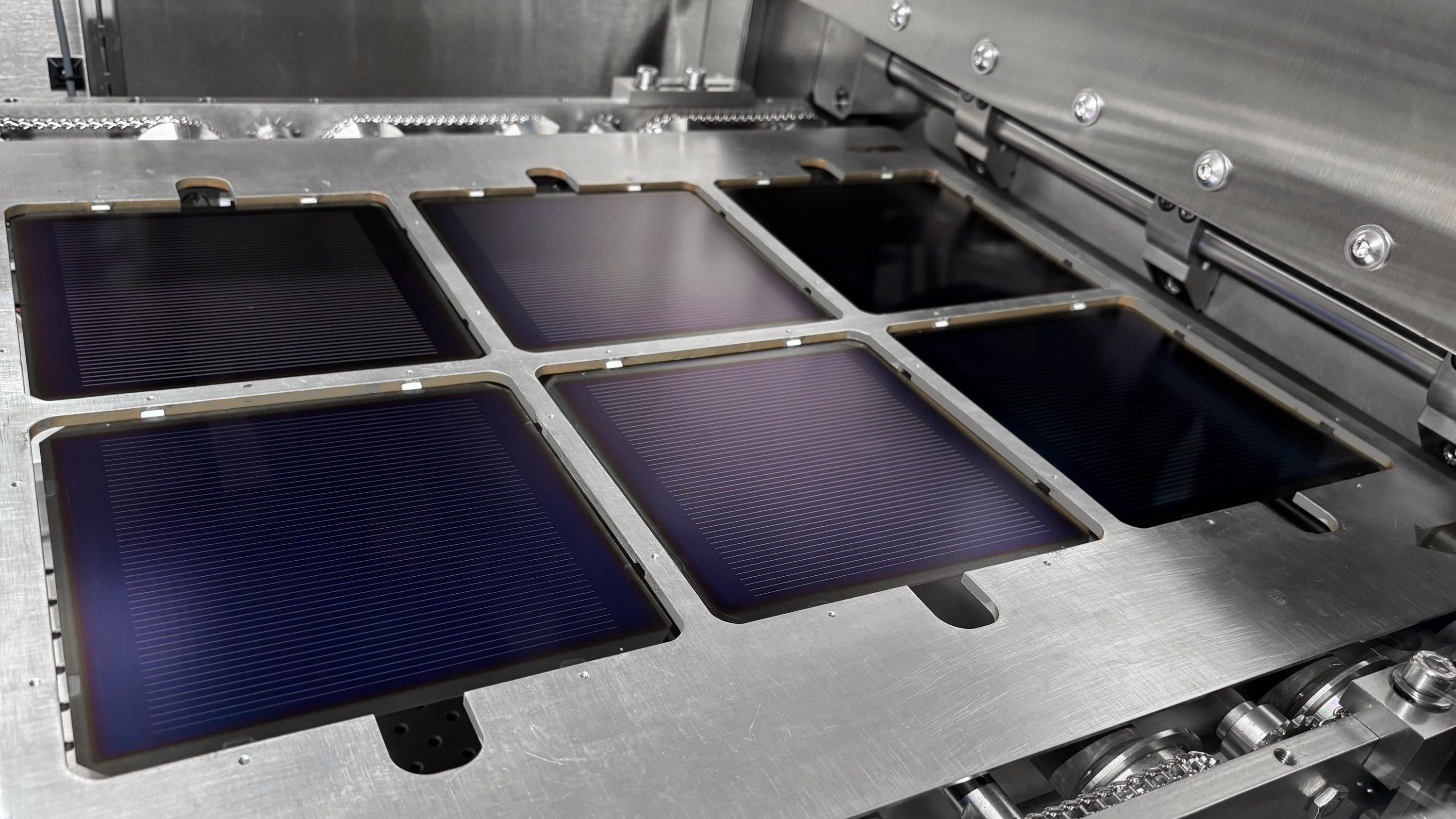

Super-efficient solar cells are on our list of the 10 Breakthrough Technologies of 2024. (If you haven’t seen that list, you can find it here!) By sandwiching other materials with traditional silicon, tandem perovskite solar cells could help cut solar costs and generate more electricity.

Hertz was billing itself as a leader in renting out electric vehicles (remember that Tom Brady commercial?). Now the company is selling off a third of its EV fleet. (Tech Crunch)

A mountain of clothes accumulated in the desert in Chile. Then it caught fire. This is a fascinating deep dive into the problem of textile waste. (Grist)

New uranium mines will be the first to begin operations in the US in eight years. The mines could help bring more low-carbon nuclear power to the grid, but they’re also drawing sharp criticism. (Inside Climate News)

Researchers at Microsoft and a US national lab used AI to find a new candidate material for batteries. It could eventually be used in batteries to reduce the amount of lithium needed to build them.(The Verge)

→ I talked about this and other science news of the week on Science Friday. Give it a listen! (Science Friday)

Animals are always evolving. A few lucky ones might even be able to do it fast enough to keep up with climate change. (Hakai Magazine)

All that new renewable energy coming onto the grid is helping make a dent in US emissions. Buildout of clean energy cut greenhouse-gas emissions by nearly 2% in 2023. (Canary Media)

The Biden administration will fine oil and gas companies for excess methane emissions. Penalties for emitting this super-powerful greenhouse gas are part of the landmark climate bill passed in 2023. (New York Times)

Texas has had a host of upgrades to its electric grid in the years since a powerful storm devastated the state in 2021. Now experts are watching to see how the grid holds up against cold weather this week. (Washington Post)

For more than a month in total, 12 metric tons of molten salt coursed through pipes at Kairos Power in Albuquerque, New Mexico.

The company is developing a new type of nuclear reactor that will be cooled using this salt mixture, and its first large-scale test cooling system just completed 1,000 hours of operation in early January. This is the second major milestone for Kairos in recent weeks. In December, the US Nuclear Regulatory Commission granted a construction permit for the company’s first nuclear test reactor.

Nuclear power plants can provide a steady source of carbon-free energy, a crucial component in addressing climate change. But recent major nuclear installations have been plagued by delays and skyrocketing budgets. Kairos and other companies working on advanced reactor designs hope to revive hopes for nuclear power by presenting a new version of the technology that could cut costs and construction times.

Kairos’s technology and construction approach are “just fundamentally different” from current commercial reactors, says Edward Blandford, cofounder and chief technology officer of Kairos.

Today, nearly all commercial nuclear plants use the same type of enriched uranium as fuel to generate electricity through nuclear fission reactions, and temperature is controlled with a cooling system that uses water.

But a growing number of companies are working to tweak this formula in an effort to improve on cost and safety. In the case of Kairos, the company plans to use an alternative fuel called TRISO, which is made from tiny uranium-containing kernels that can be embedded in graphite casings. TRISO fuel is robust, able to resist high temperatures, radiation, and corrosion. In addition, the reactor’s cooling system uses molten salt instead of water.

Molten salt could be a huge help in making safer nuclear plants, Blandford says. The cooling system in water-cooled reactors needs to be kept at high pressure to ensure that the water doesn’t boil off, which would leave the reactor without coolant and in danger of overheating and running out of control. It’s technically possible to boil salt, but it could only happen at very high temperatures. So those high pressures become unnecessary.

Molten-salt nuclear reactors were developed in the 1950s but were largely shelved as the industry moved toward water-cooled designs. Now, with a growing need for low-carbon power, “there’s a lot of interest in these technologies again,” says Jessica Lovering, cofounder and executive director of the Good Energy Collective, a policy research organization that advocates for the use of nuclear energy. New reactor technology options could help avoid some of the fears around the safety of water-cooled reactors, and they can also generate electricity more efficiently.

Technology has changed a lot in the past seven decades, and molten-salt reactors never made it to large-scale commercial operation. So there’s still plenty of testing to be done before this kind of cooling system can be put to work in the highly controlled environment of a nuclear reactor. That’s where Kairos’s engineering test unit comes in. It’s the world’s largest system built to circulate Flibe, a fluoride-based salt coolant.

The system uses electric heaters to simulate the heat that would be generated by nuclear reactions in the finished reactor. Tests involve pumping a Flibe mixture through a cooling loop while engineers monitor the temperature throughout the system and the purity of the salt along the way. The company has also tested what it would be like to refuel the reactor, and how power coming out of the system can be monitored and adjusted.

Building an entire cooling system that won’t ever be used in a nuclear reactor is a considerable investment of time, money, and resources, but this approach of taking baby steps could help Kairos succeed in introducing a new nuclear technology—a historically difficult task, says Patrick White, research director at the Nuclear Innovation Alliance, a nonprofit think tank.

“One of the challenges with nuclear is that usually, the first step is to design the reactor on paper, and the next step is build the whole thing,” White says. Kairos is trying a different path, testing out components more along the way to help speed up development and avoid getting stuck in late-stage construction.

Kairos is making progress on construction, too. The company received approval in December from the NRC to build Hermes-1, its first nuclear test reactor. Hermes-1 will produce about 35 megawatts of thermal power (today’s commercial reactors typically produce around 1,000 megawatts of electricity). It’s planned for completion as soon as 2026.

Several other companies are also using molten salt or TRISO fuel in their advanced nuclear designs. X-energy, based in Maryland, is developing a gas-cooled reactor that uses TRISO fuel, and TerraPower and GE Hitachi Nuclear Energy are developing a sodium-cooled reactor that uses molten salt to store energy.

There’s still a long road ahead before Kairos’s design and other advanced reactors can make it onto the grid. The company plans to build at least two more large-scale test cooling systems before putting the pieces together for Hermes-1, Blandford says.

The company will also need to win an operating license for Hermes-1, the second of two major regulatory steps it’ll go through with the NRC. Next comes Hermes-2, which will include two reactors that are similar in scale and design to Hermes-1, plus a system to transform the heat generated into electricity. Finally, the company will move on to larger, commercial-scale reactors.

All of that will take some time, but Kairos and others feel the result will be worth it. “With our technology, it is unique,” Blandford says, “and it does open up unique opportunities to explore spaces that other technologies have not.”

MIT Technology Review’s What’s Next series looks across industries, trends, and technologies to give you a first look at the future. You can read the rest of our serieshere.

It’s a turbulent time for offshore wind power.

Large groups of turbines installed along coastlines can harness the powerful, consistent winds that blow offshore. Given that 40% of the global population lives within 60 miles of the ocean, offshore wind farms can be a major boon to efforts to clean up the electricity supply around the world.

But in recent months, projects around the world have been delayed or even canceled as costs have skyrocketed and supply chain disruptions have swelled. These setbacks could spell trouble for efforts to cut the greenhouse-gas emissions that cause climate change.

The coming year and beyond will likely be littered with more delayed and canceled projects, but the industry is also seeing new starts and continuing technological development. The question is whether current troubles are more like a speed bump or a sign that 2024 will see the industry run off the road. Here’s what’s next for offshore wind power.

Speed bumps and setbacks

Wind giant Ørsted cited rising interest rates, high inflation, and supply chain bottlenecks in late October when it canceled its highly anticipated Ocean Wind 1 and Ocean Wind 2 projects. The two projects would have supplied just over 2.2 gigawatts to the New Jersey grid—enough energy to power over a million homes. Ørsted is one of the world’s leading offshore wind developers, and the company was included in MIT Technology Review’s list of 15 Climate Tech Companies to Watch in 2023.

The shuttered projects are far from the only setback for offshore wind in the US today—over 12 gigawatts’ worth of contracts were either canceled or targeted for renegotiation in 2023, according to analysis by BloombergNEF, an energy research group.

Part of the problem lies in how projects are typically built and financed, says Chelsea Jean-Michel, a wind analyst at BloombergNEF. After securing a place to build a wind farm, a developer sets up contracts to sell the electricity that will be generated by the turbines. That price gets locked in years before the project is finished. For projects getting underway now, contracts were generally negotiated in 2019 or 2020.

A lot has changed in just the past five years. Prices for steel, one of the most important materials in turbine construction, increased by over 50% from January 2019 through the end of 2022 in North America and northern Europe, according to a 2023 report from the American Clean Power Association.

Inflation has also increased the price for other materials, and higher interest rates mean that borrowing money is more expensive too. So now, developers are arguing that the prices they agreed to previously aren’t reasonable anymore.

China stands out in an otherwise struggling landscape. The country is now the world’s largest offshore wind market, accounting for nearly half of installed capacity globally. Quick development and rising competition have actually led to falling prices for some projects there.

Growing pains

While many projects around the world have seen setbacks over the last year, the problems are most concentrated in newer markets, including the US. Problems have continued since the New Jersey cancellations—in the first weeks of 2024, developers of several New York projects asked to renegotiate their contracts, which could delay progress even if those developments end up going ahead.

While over 10% of electricity in the US comes from wind power, the vast majority is generated by land-based turbines. The offshore wind market in the US is at least a decade behind the more established ones in countries like the UK and Denmark, says Walt Musial, chief engineer of offshore wind energy at the US National Renewable Energy Laboratory.

One open question over the next year will be how quickly the industry can increase the capacity to build and install wind turbines in the US. “The supply chain in the US for offshore wind is basically in its infancy. It doesn’t really exist,” Jean-Michel says.

That’s been a problem for some projects, especially when it comes for the ships needed to install wind turbines. One of the reasons Ørsted gave for canceling its New Jersey project was a lack of these vessels.

The troubles have been complicated by a single century-old law, which mandates that only ships built and operated by the US can operate from US ports. Projects in the US have worked around this restriction by operating from European ports and using large US barges offshore, but that can slow construction times significantly, Musial says.

Tax credits are providing extra incentive to build out the offshore wind supply chain in the US. Existing credits for offshore wind projects are being extended and expanded by the Inflation Reduction Act, with as much as 40% available on the cost of building a new wind farm. However, to qualify for the full tax credit, projects will need to use domestically sourced materials. Strengthening the supply chain for those materials will be a long process, and the industry is still trying to adjust to existing conditions.

Still, there are some significant signs of progress for US offshore wind. The nation’s second large-scale offshore wind farm began producing electricity in early January. Several areas of seafloor are expected to go up for auction for new development in 2024, including sites in the central Atlantic and off the coast of Oregon. Sites off the coast of Maine are expected to be offered up the following year.

But even that forward momentum may not be enough for the nation to meet its offshore wind goals. While the Biden administration has set a target of 30 gigawatts of offshore wind capacity installed by the end of the decade, BloombergNEF’s projection is that the country will likely install around half that, with 16.4 gigawatts of capacity expected by 2030.

Technological transformation

While economic considerations will likely be a limiting factor in offshore wind this year, we’re also going to be on the lookout for technological developments in the industry.

Wind turbines still follow the same blueprint from decades ago, but they are being built bigger and bigger, and that trend is expected to continue. That’s because bigger turbines tend to be more efficient, capturing more energy at a lower cost.

A decade ago, the average offshore wind turbine produced an output of around 4 megawatts. In 2022, that number was just under 8 MW. Now, the major turbine manufacturers are making models in the 15 MW range. These monstrous structures are starting to rival the size of major landmarks, with recent installations nearing the height of the Eiffel Tower.

In 2023, the wind giant Vestas tested a 15 MW model, which earned the distinction of being the world’s most powerful wind turbine. The company received certification for the design at the end of the year, and it will be used in a Danish wind farm that’s expected to begin construction in 2024.

In addition, we’ll likely see more developments in the technology for floating offshore wind turbines. While most turbines deployed offshore are secured in the seabed floor, some areas, like the west coast of the US, have deep water offshore, making this impossible.

There’s a wide variety of platform designs for floating turbines, including versions resembling camera tripods, broom handles, and tires. It’s possible the industry will start to converge on one in the coming years, since standardization will help bring prices down, says BloombergNEF’s Jean-Michel. But whether that will be enough to continue the growth of this nascent industry will depend on how economic factors shake out. And it’s likely that floating projects will continue to make up less than 5% of offshore wind power installations, even a decade from now.

The winds of change are blowing for renewable energy around the world. Even with economic uncertainty ahead, offshore wind power will certainly be a technology to watch in 2024.

Scientists are loudly warning that the world is running out of time to avoid dangerous warming levels. The picture is grim. But if you know where to look, there are a few bright spots shining through the darkness.

New technologies that can help address climate change, from heat pumps to solar panels to EVs, are coming to the market and getting cheaper. Climate policy is also developing, from incentives to support new technology to rule-making around pollution. And efforts to help the most vulnerable nations adapt to climate change are growing.

Here are a few of those bright spots that our climate reporters saw in 2023.

The brakes are off for electric vehicles

There’s been a spate of good news for EVs. We put the “inevitable EV” on our list of 10 Breakthrough Technologies in January, noting that strong policy support and expanding supply chains were combining to vault the technology to new relevance.

Those trends have largely continued through 2023, and that means good news for climate change, since the transportation sector accounts for nearly 20% of global emissions.

EVs are on track to make up 15.5% of automotive sales this year, according to BNEF. Between battery electric vehicles and plug-in hybrids, this new growth means there are almost 41 million passenger EVs on the road. China has the largest share of EVs in the world, making up nearly a quarter of the global fleet.

Batteries to power all those vehicles are becoming more widely available and cheaper. Global manufacturing for lithium-ion batteries increased by over 30% this year. And while prices ticked up slightly last year, they are down again in 2023, representing the largest annual decline since 2018.

A wide range of policies could help continue the growth of electric vehicles. Some governments are mandating the switch away from fossil-fuel-powered cars—the European Union and United Kingdom both passed policies in 2023 mandating that all new passenger vehicles sold be zero-emissions starting in 2035. Several states in the US have adopted the same policy, with California leading the way last year and more signing on in 2023.

Incentives are also driving consumers toward EVs. The Inflation Reduction Act in the US serves up a huge menu of tax credits for battery manufacturing, EV manufacturing, and mineral processing.

While many signs are positive, it’s not all rosy for electric vehicles. Growth in sales slowed between 2022 and 2023, and changing demand has some automakers slowing production for models like the Ford F-150 Lightning. Charging infrastructure isn’t available or reliable enough in most markets, a problem that has become one of the biggest barriers to EV adoption.

Cars are being sold at a record pace and road emissions are still going up, so EV sales need to accelerate to make a dent in transportation’s climate impact. But EVs’ progress so far seems to be an encouraging story of a new climate-friendly technology becoming a mainstream option. Let’s hope it keeps going in 2024—all gas, no brakes.

—Casey Crownhart

Countries and companies are cracking down on methane

Another encouraging development on the otherwise daunting topic of climate change is the growing recognition that cutting methane pollution is one of the most powerful levers we can pull to limit global warming over the coming years.

Carbon dioxide has long overshadowed methane, since we emit so much more of it. But methane traps about 80 times as much heat over a 20-year period and accounts for at least a quarter of overall warming above our preindustrial past.

On the other hand, it also breaks down far faster in the atmosphere. Together, those qualities mean that rapid cuts in methane emissions today could deliver an outsize impact on climate change, potentially shaving a quarter-degree off total warming by midcentury. That could easily make the difference between a planet that does or doesn’t tip past 2 °C.

So it was encouraging to finally hear the head of the US Environmental Protection Agency announce, at the recent UN climate conference, that it will soon require oil and gas companies to monitor methane emissions across their pipelines, wells, and facilities and sharply reduce venting, flaring, and leaks.

As federal regulations go, preventing emissions of a combustible, planet-warming superpolllutant that isn’t even producing anything of economic value is truly about the least we can ask of an industry. But it’s a step forward that promises to eliminate the warming equivalent of about 1.5 billion metric tons of carbon dioxide by 2038.

There was other good news on methane at the UN conference as well. A group of major oil and gas companies including BP, Exxon, and Saudi Aramco pledged to cut their methane pollution by at least 80% by 2030. In addition, a handful of additional nations joined an international coalition committed to easing global emissions by 30% this decade, while others stepped up their pledges and funding.

All of this comes on top of growing global efforts to more effectively monitor and report major sources of methane pollution around the globe, and reduce emissions from agriculture and landfills.

As with every issue when it comes to climate change, none of this is enough, too much of it is voluntary, and complications abound. But these announcements, along with other signs of progress, are slowly adding up to a less grim future, while reminding us all that we’re capable of achieving even more.

—James Temple

A crucial fund to pay for climate damages launched

While the world scrambles to slow our emissions, it’s becoming ever more clear that the damage from climate change is happening in the present tense, with wildfires, floods, and heat waves making headlines.

So it was welcome news that this year’s UN climate conference started with a historic milestone for vulnerable countries struggling to deal with these problems. On day one of the talks, the long-anticipated loss and damage fund was officially launched.

Historically, a handful of industrialized nations like the United States, Germany, and the United Kingdom have been responsible for much of the emissions that are exacerbating extreme weather events and related disasters. Now, they are (nominally) paying for that legacy.

The purpose of this fund is to help poor and developing countries address the increasing harm from climate disasters. Many of these countries—which have contributed the least amount of emissions—are the most vulnerable to climate impacts and often lack adequate resources to manage them. The funds can help them rebuild in the aftermath of events like drought or floods, and improve a nation’s ability to withstand future catastrophes.

Advocates have been quick to point out that the total amount pledged so far is minuscule compared to the actual need on the ground. They estimate that the current pledge equates to less than 0.2% of the potential economic losses facing developing nations from climate disasters every year.

By the end of COP28 on December 12, countries had collectively committed nearly $800 million. The United Arab Emirates and Germany each pledged $100 million, the United Kingdom offered $75 million, and the United States contributed $17.5 million.

Those numbers sound big, but a fewpeople have made a sports analogy that puts this all in perspective. On December 9, a baseball player, Shohei Ohtani, signed a $700 million contract with the LA Dodgers. The fact that a worldwide effort to address climate change is even remotely comparable to the amount spent by a sports team on a single athlete should be a global embarrassment.

“The rich world needs to take a good look at itself and its actions so far,” says Ritu Bharadwaj, a principal researcher at the International Institute for Environment and Development.

That being said, the fund is still a step toward equitable climate resilience. Now the focus is on continuing to scale up the commitments and making the funds more accessible to those who need them.

Lost in a stupor of déjà vu, I rang the intercom buzzer a second time. I had the odd sensation of being unstuck in time. The headquarters of this solar startup looked strangely similar to its previous offices, which I had visited more than a decade before. The name of the company had changed from 1366 Technologies to CubicPV, and it had moved about a mile away. But the rest felt familiar, right down to what I had come to talk about: a climate-tech boom.

A surge in cleantech investments, which had begun in 2006 with the high-profile entry of some of Silicon Valley’s leading venture capitalists, was still going strong during my first visit, in 2010—or at least it seemed to be. But a year later, it had begun to collapse. The rise of fracking was making natural gas cheap and abundant. US government funding for clean-energy research and deployment was falling. Meanwhile, China had begun to dominate solar and battery manufacturing. By the end of 2011, almost all the renewable-energy startups in the US were dead or struggling to survive.

The list of eventual casualties included headline grabbers like the solar-cell maker Solyndra and the high-flying battery company A123, as well as numerous less well-known startups in areas like advanced biofuels, innovative battery tech, and solar power. How, I was wondering, had CubicPV survived when nearly all its peers had failed?

Ushering me into the conference room (was that the same photo of a solar panel hanging on the wall that I had seen a decade before?), Frank van Mierlo, who is still the CEO, seemed almost giddy. And why not? After more than 10 years in photovoltaic limbo, with few opportunities to scale up its process for making the silicon wafers used in solar cells, the venture-backed company had suddenly seen its fortunes turn around.

The excitement around cleantech investments and manufacturing is back, and the money is flowing again. The 2022 US Inflation Reduction Act, which provides strong incentives for US domestic solar manufacturing, changed everything, says van Mierlo. As of this summer, some 44 new US plants had been planned, providing CubicPV with a huge potential demand for its silicon wafers.

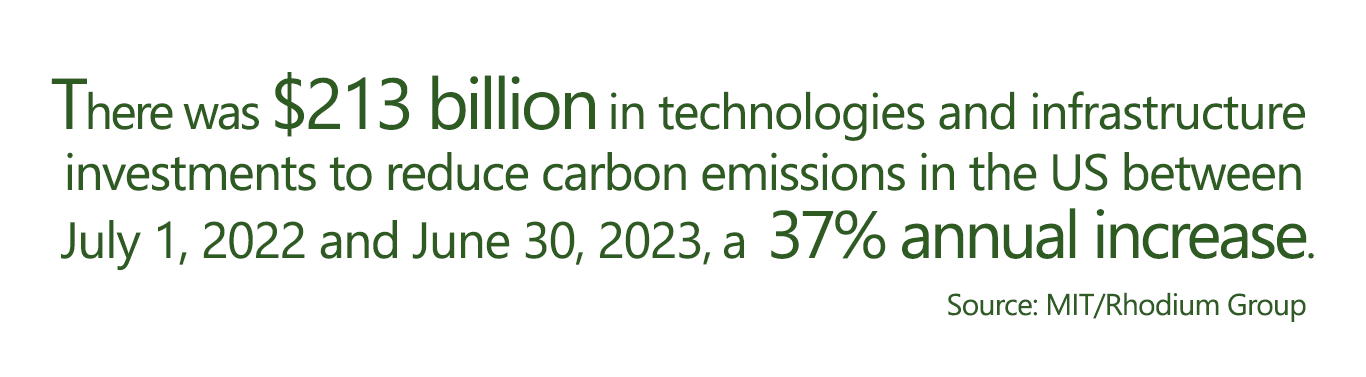

Call it cleantech 2.0. In recent years, there has been a huge increase in public and private spending, both in the US and elsewhere, on technologies and infrastructure to address climate change. A recent analysis estimates that total green investments reached $213 billion in the US during the 12 months beginning July, 2022. Most of that spending is allocated to building sources of renewable energy, such as wind or solar, as well as to supporting battery and EV manufacturing and creating green hydrogen infrastructure. And the enormous amount of money is creating potential opportunities for the next generation of technologies to feed the expanding markets.

For startups like CubicPV, this means that after years of little market demand, the appetite for its products is suddenly almost insatiable. The company is designing a billion-dollar plant to make the silicon wafers needed to feed the rapid expansion in US solar production. What’s more, a bigger solar manufacturing base could eventually provide the startup with a lucrative future market for its next innovation: a new type of solar panel that is far more efficient at capturing sunlight than conventional silicon ones.

Silicon Valley and venture capitalists everywhere have fallen in love with the virtues and the promise of new catalysts and electrodes. Innovations in solar cells no longer seem like a lost cause. Startups are boasting radical new technologies for energy storage and carbon-free processes for making chemicals, steel, and cement. Investors are risking billions on scaling up nascent technologies such as geothermal power, fusion reactors, and ways to capture carbon dioxide directly from the air.

These innovations in what is being called “deep” or “hard” tech—products and processes based on science and engineering advances—could be critical in addressing climate change. While the past few years have seen remarkable progress in deploying relatively mature renewables such as solar and wind power, as well as strong growth in electric-vehicle sales, large gaps in the cleantech portfolio remain. In its most recent report this fall, the International Energy Agency estimates that around 35% of the emissions cuts needed to meet 2050 climate goals will have to come from technologies not yet available.

Key industrial sectors of the economy, in particular, have largely been untouched. Nearly a third of carbon emissions come from industrial processes used to make steel, cement, chemicals, and other commodities; concrete alone accounts for more than 7% of global emissions, while steel production is responsible for another 7% to 9%. Cleaning up these industries will take an almost unlimited supply of cheap, steady, and easily accessible carbon-free energy.

Progress will almost certainly require new science-based innovations. And that’s where venture-backed startups play an essential role. Over the last few decades, large industrial corporations in sectors such as energy, chemicals, and materials have all but abandoned research into new technologies. The days when industrial giants like DuPont created critical new technologies and spun them off into profitable operations are long gone. And while governments and universities fund research, venture-backed firms have emerged as an increasingly key outlet for transforming promising lab discoveries into sustainable businesses.

A slew of such startups are now rapidly moving toward commercialization, providing the first steps toward industrial decarbonization and adoption of radically new energy sources (see chart). But these startups still face some of the same issues that tripped up the cleantech revolution a decade ago.

Transforming academic advances in physical sciences and engineering into commercial businesses is a project that’s fraught with dangers. It typically requires startups to build so-called demonstration plants at a relatively large scale to test whether their processes work beyond the lab and are efficient enough to compete with existing technologies. This is risky and expensive. Then, if it all works, startups commercializing, say, new energy sources or low-carbon processes to make concrete or steel face low-margin, well-established markets. They must often compete with mature processes that have been optimized over many decades.

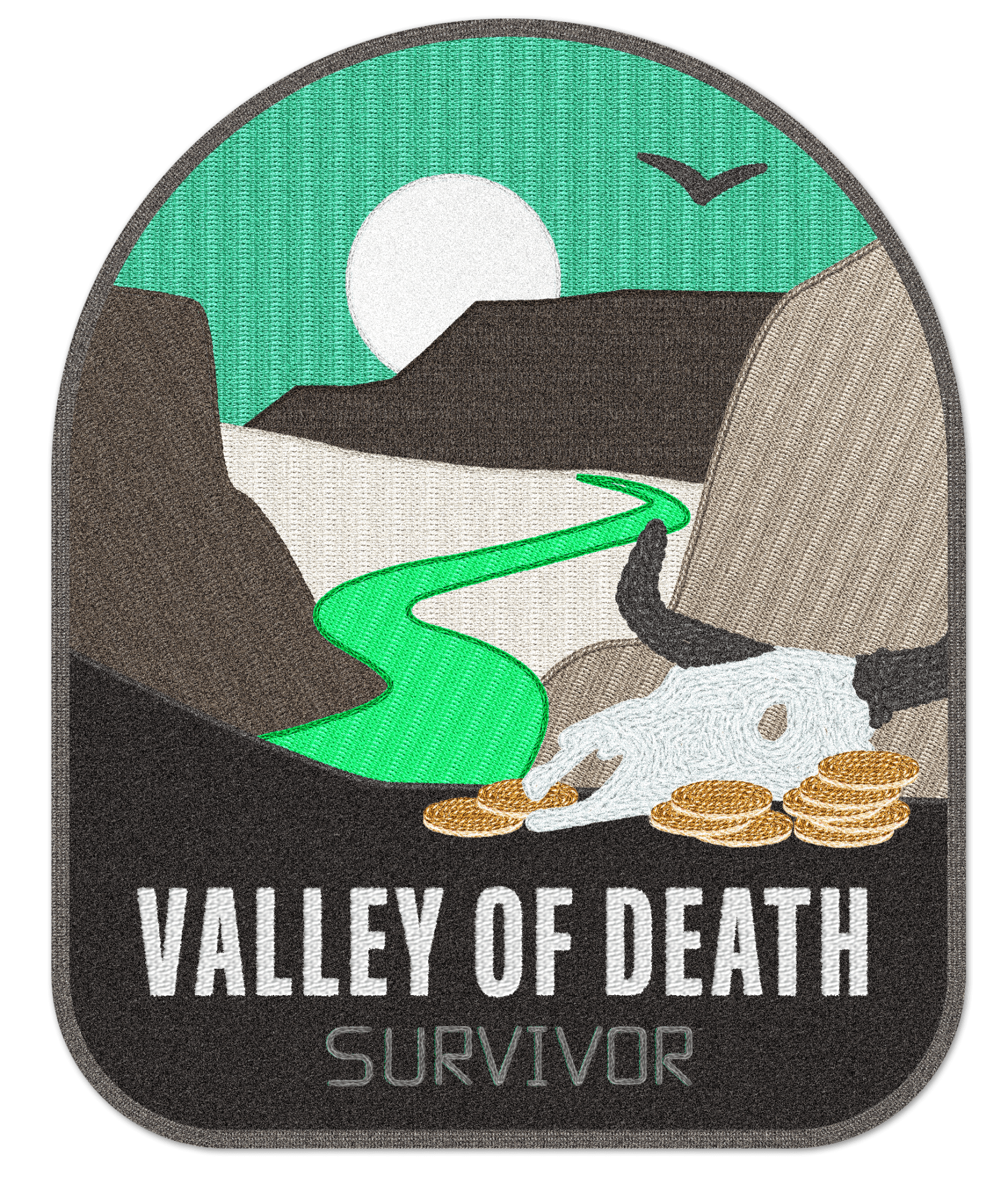

These costly and time-consuming steps to commercialization, which a climate-tech startup must survive before it has any significant revenues, is often known as the “valley of death.” Few startups in cleantech 1.0 were able to navigate it.

The question now is: Can today’s ambitious startups successfully scale up their technologies and move across that valley this time around? These fledging venture-backed companies will first need to prove that their technologies work at a commercial scale. Then, if successful, they face the even harder challenge of making an impact on the huge energy and industrial markets, figuring out how to work with established companies to clean up these sectors. Can they survive?

Born again

The bad news is that the record for such venture-backed startups is dismal. From 2006 to around 2011, when much of the sector lay in ashes, venture capitalists spent about $25 billion on cleantech startups. The VCs lost more than half their money. It was particularly bad for those firms we would now call deep-tech startups; investments in stuff like new types of solar cells, advanced biofuels, and novel battery chemistries returned only about 16 cents on a dollar.

For much of the rest of the decade, investors hunkered down. As spending on cleantech dwindled to miserly levels, consumer-facing software-based businesses (think Airbnb and Uber) took off. The common wisdom was that advances based on science and engineering in cleantech were too expensive and risky to scale up. The proportion of venture capital going to cleantech dropped from more than 8% in 2008 to around 3% between 2016 and 2020.

Even before the 2022 IRA passed, however, venture investors had again begun eyeing the massive potential markets for climate tech, as governments around the world increased spending and more and more corporations set long-term emission-reduction goals. The markets are now real and growing, not speculative. While innovative battery startups a decade ago faced a tiny market for electric vehicles, today there is a huge demand for cheaper and more powerful batteries as sales of EVs take off. Likewise, demand for grid storage is growing as more renewable power is deployed and for cleaner industrial processes as companies pledge to reduce their carbon pollution.

Yet the trajectory of climate tech in recent years hasn’t been a straight line. Venture investments in cleantech startups, which amounted to just $2 billion in 2013, soared to nearly $30 billion in the US by 2021, according to the National Venture Capital Association. Then, just as things started to heat up, inflation and the resulting rise in interest rates began to make borrowing money expensive. The general venture capital market began to crash in 2022, and investments in climate tech soon followed. In the first half of 2023, investments in climate-tech startups were down 40% from the same period in 2022, reports Sightline Climate, a market intelligence firm.

But dig deeper into the numbers and a mixed picture emerges. For one thing, Sightline Climate says investments have begun creeping back up in the latest quarter this fall. And though funding overall became more difficult to secure in the first half of 2023, some companies—especially in markets favored by the IRA legislation, like green hydrogen, batteries, solar, and carbon capture from the air—are still raising large amounts of money. According to the latest data from the Engine, a “tough tech” venture group spun out of MIT, VC investments in startups working on industrial chemicals, materials, and carbon capture were actually up in the first half of 2023 from the same period in 2022—in fact, they were nearly at 2021 levels.

For some startups, however, readily available cash has dried up, providing a reality check on their sustainability. And the first few failures could raise the ghosts of cleantech 1.0. But for many others, the financial downturn is simply the most recent reminder that climate-tech investments aren’t exempt from swings in the health of the economy.

The same fundamental challenge that venture-backed startups faced in commercializing transformative technologies 15 years ago still exist. Novel, gee-whiz tech is not enough; a clear plan to target well-defined markets remains key to survival. “What is the path to market for these technologies?” asks David Popp, an economist at Syracuse University. He attributes the collapse of startups in cleantech 1.0 largely to the lack of demand for green products in highly competitive commodity markets. And that business puzzle, he says, remains: “I’m kind of curious to see, looking back five years from now, whether we’ll be looking at this like the first cleantech bubble.”

New money. Old problems.

In an influential 2016 post-mortem of cleantech 1.0 by the MIT Energy Initiative, several researchers analyzed what went wrong and concluded that venture capital was “the wrong model for clean energy innovation,” putting the blame on VCs’ unsuccessful attempts to fund startups through the “valley of death” by themselves. Simply put, the VCs quickly ran out of money and patience. The report’s conclusion: “The sector requires a more diverse set of actors and innovation models.”

The good news is that the types of investors funding cleantech have in fact become more diversified. Arguably the biggest difference is that VCs are no longer going it alone. Thanks to the huge potential markets in renewable power and industrial decarbonization, there is a growing appetite among other types of investors to fund expensive and risky scale-up projects.

Many of these investing groups, which includes hedge funds, corporations, growth investors, and even wealthy individuals, can readily write checks for $100 million or $200 million, and today they’re providing much of the funding for the flurry of demonstration plants. “There is a whole new generation of investors whose entire business is financing first deployment to nth deployment,” says Matthew Nordan, general partner at Azolla Ventures. “That didn’t exist before, and that is where many of the [earlier] companies died on the shoals.”

The new investors include companies in sectors such as steel, chemicals, and concrete that are bracing for an inevitable long-term shift to lower-carbon processes. Typically led by their venture groups, these corporations—such as steel manufacturer ArcelorMittal and Siam Cement Group, a conglomerate based in Bangkok—are supporting startups in their areas of business with financing and engineering expertise. And though their commitment to investing in climate-tech startups is sometimes viewed with skepticism, the money is real—and so is the time and expertise they’re bringing to the new technologies.

Still, Francis O’Sullivan, one of the authors of the 2016 MIT report who is now a lead climate investor at S2G Ventures, says that the way the startups are funded remains broken. The problem now, O’Sullivan says, is that the money is in several different types of buckets. There is a huge amount of money going to early-stage startups. And there is also ample money from banks and institutional investors for so-called infrastructure spending on well-proven technology (such as building a new wind or solar farm). But the bucket of money for the critical “growth stage”—funding for the demonstration of first-of-a-kind technologies—is relatively small.